Judgment Road

The road to judgment is often longer than people think.

Lets all agree…being in debt collection is not fun.

With many Americans living paycheck to paycheck, the threat of debt collection is a tangible fear — or reality. But what really happens in debt collection? This short article explains what happens in collections and gives you an expected timeline for collection actions.

CAVEAT: Not all debts and not all lawsuits are created equal. The information in this article is for informational purposes only. Speak to an attorney (preferably one at Pioneer Bankruptcy) about your your specific situation.

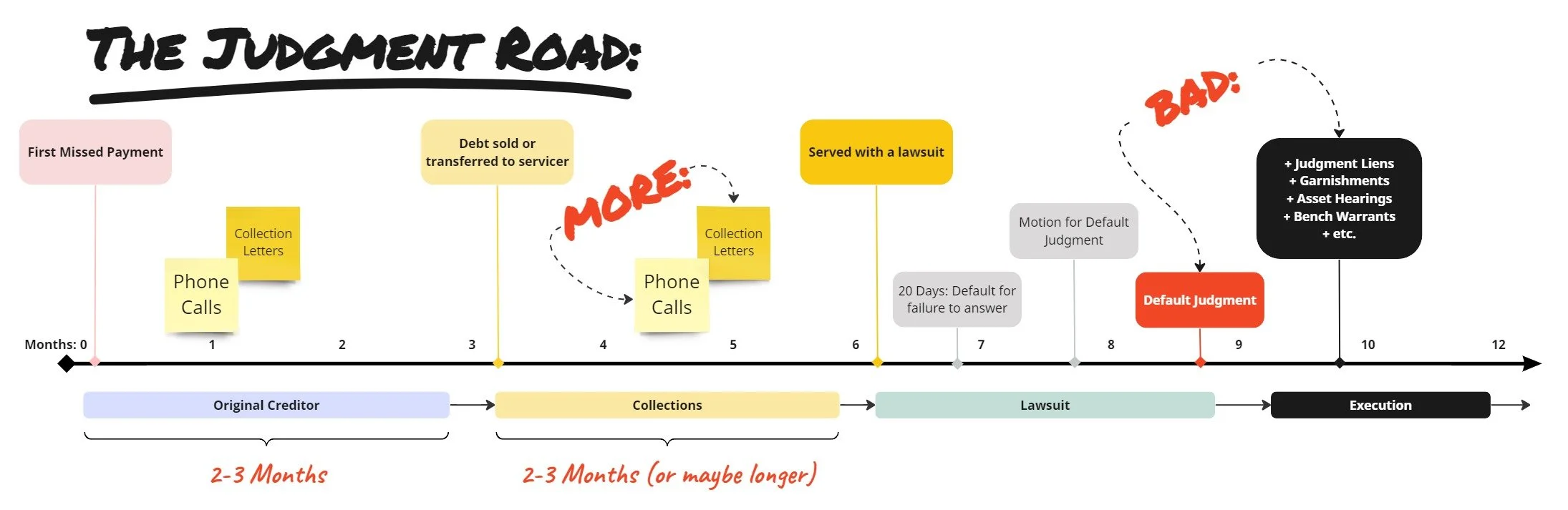

When it comes to collecting on debts, creditors will often follow a predictable pattern. This patter is illustrated in the image above. Knowing this pattern will help you navigate debt collection and prepare for what creditors might do.

The important thing to keep in mind is that Creditors cannot simply take assets from you because you owe a debt. The Creditor must have a judgment before it can take your assets (repossessions and a secured creditor’s right to self-help will be addressed in a subsequent article).

For this article, we will use a hypothetical example to help illustrate. In our example, Bob owes credit card debt of $20,000.00 to XYZ credit card company.

Phase 1 | Collection by Original Creditor | Months 0-3

When Bob misses his first monthly payment to XYZ, the collection clock begins ticking. Typically, the original creditor, XYZ, will begin attempts to urge Bob to bring the payments current or to pay of the debt for the first two to three months after Bob becomes delinquent. As part of its collections efforts, XYZ will often (1) send letters, (2) make phone calls, (3) report negatively on Bob’s credit, and (4) cut off Bob’s additional lines of credit in an attempt to goad Bob into pay the debt.

Mercifully, at this stage, XYZ likely cannot garnish Bob’s wages or try to foreclose on Bob’s home. These things can only be done after after XYZ has received a judgment at the end of a lawsuit. XYZ is just limited to harassing Bob. While the harassment is deeply distressing and embarrassing for Bob, XYZ cannot immediately take away Bob’s money and things.

After approximately two or three months of in-house collections, XYZ will likely grow tired of collecting and will transfer Bob’s account to a collection company, ABC.

Phase 2 | Collection by Collection Company | Months 4-6

In the Second Phase, a company dedicate to collections will likely take over the efforts to squeeze money out of Bob. ABC and other companies like it do nothing but collect debt. Although ABC cannot immediately go after Bob’s assets yet, they will likely be much more aggressive with (1) sending letters and (2) making phone calls. ABC will do everything it can to scare or otherwise bully Bob into a repayment plan.

How long ABC decides to collect and how aggressively it will pursue individual debtors can vary quite significantly. Some collection companies will pursue individual accounts for months if not years. To simulate an aggressive collection action, we might expect the collection company to send letters, make phone calls and otherwise try to harass Bob for at least two to three months. After three months, ABC will send Bob’s account to Larry the Lawyer.

Phase 3 | Lawsuit and Judgment | Months 7-9

After Larry the Lawyer drafts up and files the lawsuit, he must serve Bob with a copy of the Petition and Summons. Once Bob is served, the collection clock really begins to tick fast. Once receiving the Petition and Summons, Bob has twenty days to answer the allegations in the Petition. If Bob fails to respond within the twenty days, Bob will be considered “in default.”

Generally, Larry the Lawyer will file a Motion for Default Judgment against Bob thirty days after Bob’s deadline to answer expires. If Bob still does not reply, the Court will often enter a Default Judgment against Bob within fifteen to thirty days after the filing of the Motion for Default Judgment. Bob now has a court-ordered judgment against him…the creditors are now getting much closer to seizing Bob’s assets or garnishing his wages.

But, a judgment is just a piece of paper. The judgment merely describes how much Bob owes the original creditor (or successor creditor). Its what the judgment enables that should cause Bob true concern.

Phase 4 | Execution | Months 10+

Once XYZ has a judgment against Bob, it can now begin to “execute” the judgment against Bob’s assets. In Oklahoma, there are multiple ways a creditor can execute upon a debtor’s assets:

File the Judgment with the County Land Records creating a “Judgment Lien” on any land owned by the Debtor;

Garnish the Debtor’s wages or bank account;

Bring the Debtor to court for an Asset Hearing where the Debtor has to explain what assets he owns,

If A debtor fails to show up, the court will likely enter a bench warrant for the debtor’s arrest;

Garnishments, Judgment Liens and Asset Hearings are what really hit Bob where it hurts: his wallet. Oklahoma permits garnishments up to 25% of an individual’s paycheck. Judgment Liens will prevent your home from being sold unless the debt is repaid. Asset Hearings require you to appear in court with the possible threat of a bench warrant.

It is these collection actions at the very end of a lawsuit that we want to avoid most. The good thing is that it takes at least a little bit of time from the first missed payment to get to judgment execution.

As laid out in our hypothetical, the fastest a garnishment will be put in place after Bob misses his first payment is nine months. Most will take much longer.

Bankruptcy Stops the Judgment Road

Getting off Judgment Road is not an easy thing to do. One of the fastest and most certain paths of Judgment Road is bankruptcy. By filing bankruptcy, you put a stop to the whole collection process.

Although it can take awhile from the first missed payment to the first garnishment, please do not wait to consult with an experienced Chapter 7 or Chapter 13 attorney at Pioneer Bankruptcy. Each situation is unique and some bankruptcies require planning and preparation. Do not delay in seeking legal advice for dealing with any debt collection issues you face now. Give our office a call so we can begin to help you take the first available exit off Judgment Road.